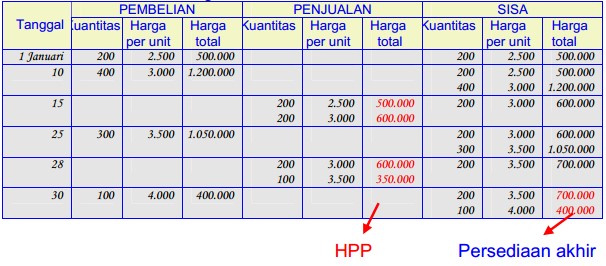

Employees feed this information into a continually adjusted database that tracks each change. The automatic, or perpetual, updating of the inventory is what gives the system its name and differentiates it from the periodic approach. Remember that under FIFO, periodic and perpetual inventory systems will always give you the same cost of goods sold and ending inventory. When calculating using the perpetual systems, do not separate purchases and sales. At the time of each sale, we must consider what units are actually available to be sold. The company has the units from beginning inventory and the purchase on January 3rd.

Information Relating to All Cost Allocation Methods, but

The cost ofgoods sold, inventory, and gross margin shown in Figure 10.13 were determined from the previously-stated data,particular to specific identification costing. Grocery stores want to sell their oldest inventory first, so it doesn’t spoil or expire. The grocery store’s approach reflects the FIFO inventory method, which assumes that the store sells its oldest inventory items first. That means that you’ll use the oldest costs to calculate the cost of goods sold. Large businesses with enormous quantities of inventory favor perpetual inventory systems. Perpetual inventory systems can also be ideal for emerging and small to medium-sized businesses looking for scalability.

What is an inventory cost flow assumption?

The company then makes a count of the physical inventory and the accountant shifts any balance in the purchases into the inventory account. Next, the accountant adjusts the inventory account to match the cost of the ending inventory. This number is critical since the company does not track unique transactions. Whether the company performs it weekly, monthly, quarterly or annually, this inventory kicks off the records reconciliation. This results in deflated net income costs in inflationary economies and lower ending balances in inventory compared to FIFO. The inventory item sold is assessed a higher cost of goods sold under LIFO during periods of increasing prices.

Last-In First-Out (LIFO Method)

- Therefore, we only need to look at the most recent purchases to determine how much our ending Inventory costs.

- As you’ve learned, the perpetual inventory system is updatedcontinuously to reflect the current status of inventory on anongoing basis.

- The Weighted Average Cost (WAC) is the cost flow assumption businesses use to value their inventory.

- The company has the units from beginning inventory and the purchase on January 3rd.

- Kristin is also the creator of Accounting In Focus, a website for students taking accounting courses.

As can be seen from above, the inventory cost under FIFO method relates to the cost of the latest purchases, i.e. $70. Average cost inventory is another method that assigns the same cost to each item and results in net income and ending inventory balances between FIFO and LIFO. Inventory is assigned costs as items are prepared for sale and based on the order in which the product was used. FIFO means “First In, First Out.” It’s an asset management and valuation method in which older inventory is moved out before new inventory comes in. Weighted Average Periodic simply takes the total costs incurred for all Raw Inventory, and weighs that on a per unit basis, at any given point in time.

Inventory Costing Approaches: FIFO and Weighted Average

On 3 January, Bill purchased 30 toasters, which cost him $4 per unit and sold 3 more units. In accounting, First In, First Out (FIFO) is the assumption that a business issues its inventory to its customers in the order in which it has been acquired. Figure 10.20 shows the gross margin, resulting from theweighted-average perpetual cost allocations of $7,253.

The FIFO Method: First In, First Out

As we discussed above, FIFO results in a higher gross profit during periods of rising prices. However, if a company used LIFO during a period of rising prices, gross profit would be lower. The key takeaway here is that when you’re calculating the cost of goods sold or ending inventory using periodic FIFO, the date on which the company sold the goods doesn’t matter. You simply assume that the oldest stock is sold first and apply this assumption to your calculations.

The accounting period can be in months, quarters or a calendar year. The COGS in a perpetual system is rolling and recalculated after each transaction, but you can use the COGS formula to calculate it for a period. When new products enter a business, life for ministers after opting out of social security employees scan them (along with their details) into the computer system. Without a computerized inventory system, it would be difficult to track every transaction in a business manually, especially in companies that sell many products.

If you want to read about its use in a perpetual inventory system, read “first-in, first-out (FIFO) method in perpetual inventory system” article. During periods of inflation, a LIFO system may be more appropriate for companies that do not wish to pay as much in taxes, because it will show a higher COGS expense and a lower net income. Therefore, your company has a lower tax liability in a LIFO system, because businesses get taxed on profit.

See the example LIFO perpetual inventory card below to get an idea of how it works. The retail sales for this product in this company were $25,000 from Jan. 1, 2019 to Jan. 15, 2019. The last-in, first-out method (LIFO) of cost allocation assumesthat the last units purchased are the first units sold. At the time of the second sale of 180 units, the LIFOassumption directs the company to cost out the 180 units from thelatest purchased units, which had cost $27 for a total cost on thesecond sale of $4,860. Thus, after two sales, there remained 30units of beginning inventory that had cost the company $21 each,plus 45 units of the goods purchased for $27 each. The lasttransaction was an additional purchase of 210 units for $33 perunit.

Leave A Comment